Africa's instant payment build-out has reached a tipping point. Twenty-five African countries now have a live domestic instant payment system, up from twenty in 2022, with another nineteen in development and the Gates Foundation backing the goal of a live system in every African country by 2030. The rails are arriving. The open question is whether they will be trusted enough to use.

That question is now the binding constraint. In its March 2026 white paper Scaling Instant Payments in Africa, AfricaNenda and its co-authors put it plainly: building the payment rail alone is not enough, and "trust is the new frontier." Drawing on payment providers across twenty African countries, the paper finds that fraud, scams and weak dispute resolution are among the biggest threats to adoption – and that the threat falls hardest on exactly the first-time and low-income users that instant payments are meant to include.

Why the timing is not negotiable

The reason to act now, rather than later, is that the decisions made at launch are extraordinarily hard to undo. As the white paper notes, policy choices on access, pricing, governance and fraud liability are path-dependent and can shape market structure for decades. A trust layer retrofitted after a fraud wave has already eroded confidence is fighting uphill against a public that has learned not to trust the channel. A trust layer designed in from the start sets the norm before the harm.

The harm curve is also unforgiving in its timing. Once funds move across a real-time rail, the window in which recovery remains realistically possible closes within twenty-four hours. Most national redress mechanisms still rely on manual call centres, paper-based routing and multi-day legal procedures to authorise a freeze – a tempo that cannot match the speed of an instant payment scam. The asymmetry between criminal velocity and institutional response is the core vulnerability, and it is widest precisely in the early months of a new system.

What a trust layer actually is

A trust layer is not a single product bolted onto a payment switch. As set out in Proto and FNA's blueprint, Redress and Fund Recovery in Digital Public Infrastructure, it is three integrated functions operating under a central bank mandate:

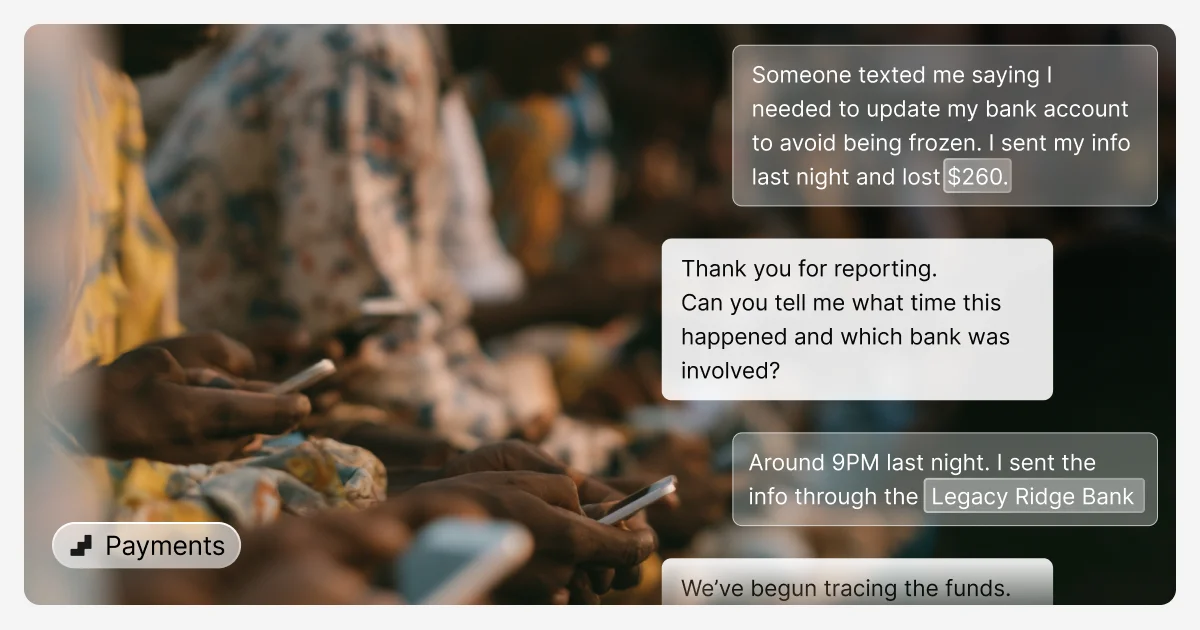

- Redress – zero-cost grievance intake through messaging apps, SMS, webchat and voice, in local languages, with AI-mediated resolution and automatic escalation of scam reports.

- Recovery – real-time, cross-institution tracing of funds, with a time-limited administrative freeze delegated to an anti-scam centre and KYC-verified return to victims.

- Instant payment integration – a federated model in which each institution keeps sovereignty over its data while contributing the fraud signals and case metadata that make tracing possible.

Crucially, the blueprint pairs this with a liability waterfall – a funding model that transitions from donor capital to a self-sustaining basis and ensures the cost of protection never falls on low-income consumers. This directly answers the white paper's warning that mandating "free" payments without a clear funding model simply hides the cost and weakens the system.

The redress workflow is ready to deploy

The encouraging part is that this is not theoretical. The AfricaNenda paper points to online dispute resolution as the only scalable way to handle the volume of disputes a live instant payment system generates, and to national anti-scam centres – on the Singapore model, where the central bank, police and telcos act together – as the proven institutional pattern.

Proto has the redress workflow ready to go: AI agents that intake a complaint in local languages, generate a structured case, route it to the responsible institution automatically, and escalate scam reports to track-and-trace within the recovery window. It is the same architecture already operating with central banks and regulators across emerging markets, deployed today in the National Bank of Rwanda's eKash environment built on open-source rails.

The rails are being laid across the continent right now. The moment to build the trust layer into them – not after them – is now.